With 30-year mortgage rates hovering around 6.65%, many potential homebuyers are wondering whether now is the right time to buy or if they should wait for rates to drop.

While it’s natural to hope for lower rates, waiting could cost you more in the long run. Home prices in Central Ohio continue to rise, and experts predict that demand will remain strong. If you delay, you may face higher home prices and increased competition, making it even tougher to find the right home at the right price.

Let’s take a closer look at why buying now may be the better financial move.

The Reality of Mortgage Rates & Home Prices

It’s understandable that homebuyers want to secure the lowest possible mortgage rate, but trying to time the market can backfire. While some forecasts suggest that rates may gradually decline to 6.4% in 2026, that small difference is unlikely to outweigh the rising home prices and increased competition expected in Central Ohio’s housing market.

Central Ohio Housing Market Trends

Columbus and the surrounding areas remain one of the hottest real estate markets in the U.S., and the data supports it:

More Homes on the Market – Inventory has increased by 21% compared to last year, giving buyers more choices right now.

Home Prices Keep Climbing – The median home price in Columbus reached $315,665 as of December 2024, a 3.3% increase from last year—and prices are expected to keep rising.

High Demand & Market Competitiveness – Columbus is ranked No. 12 among the most competitive housing markets in the country. Homes are selling fast, and values are likely to continue appreciating.

Why Buying Now Makes Financial Sense

If you’re holding off on buying in hopes of lower mortgage rates, consider this:

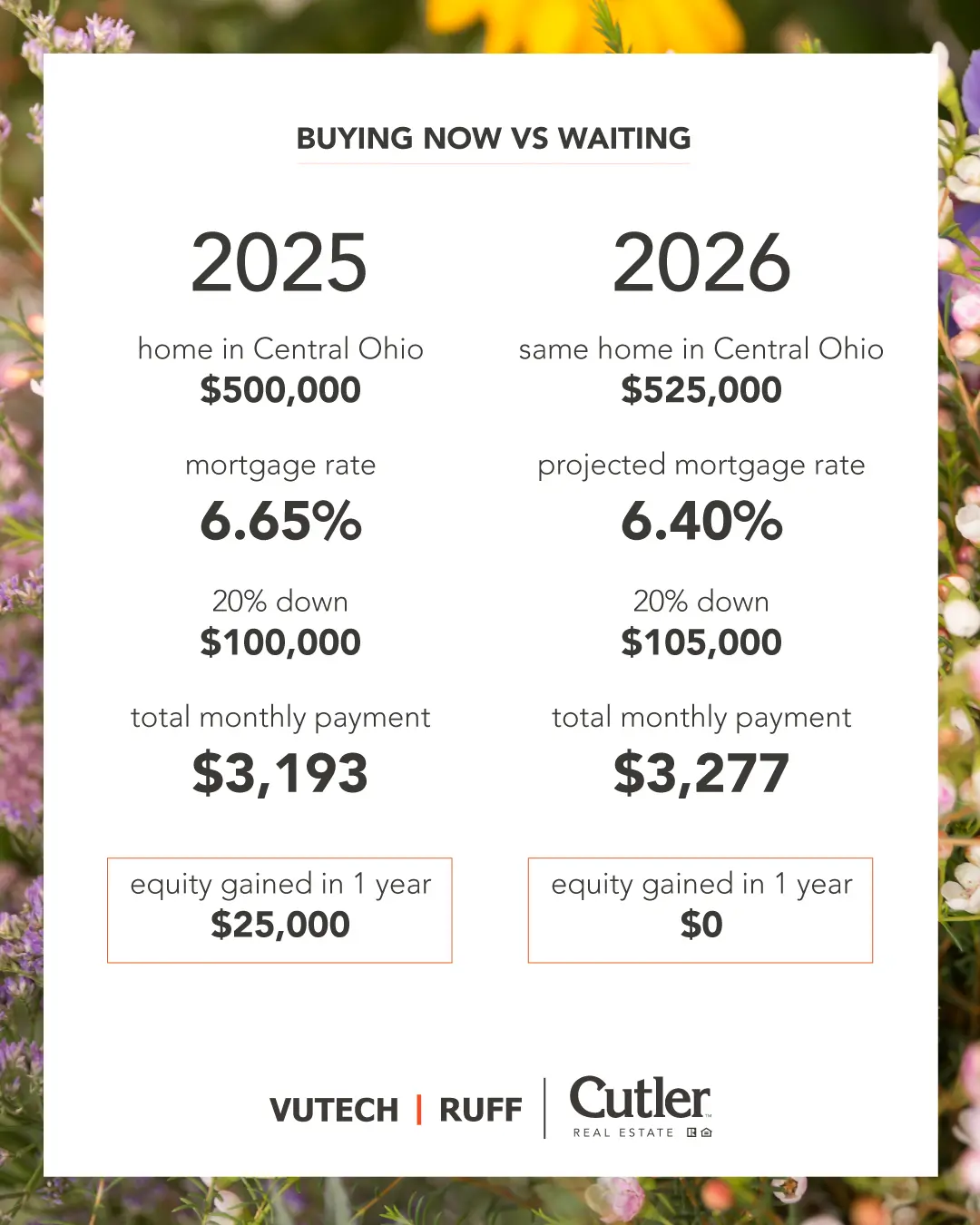

Home Prices Are Rising Faster Than Rates Are Dropping

While some forecasts suggest mortgage rates may decline slightly to 6.4% in 2026, the difference is minimal compared to the expected rise in home prices.

For example, a $500,000 home in 2025 could be worth $525,000 in 2026, meaning you’d pay $25,000 more for the same property if you wait. Even if rates improve slightly, your overall loan amount will be higher, leading to a potentially larger monthly payment.

More Inventory, Less Competition … For Now

Right now, buyers have more choices and slightly less competition. But as inventory tightens again, bidding wars could return, making it harder to secure your ideal home.

You Can Always Refinance Later

One of the biggest misconceptions about mortgage rates is that you’re stuck with them forever. If rates drop in the future, you can refinance—but you can’t go back in time to buy at today’s lower prices.

Now is the Time to Buy

The Columbus real estate market remains strong, and while mortgage rates are a factor to consider, home prices and market conditions matter even more. Instead of waiting and risking a higher purchase price and more competition, buying now allows you to lock in a home at today’s value, start building equity, and refinance later if rates improve.

At Vutech | Ruff, we believe that every home purchase should be an inspired move—one that aligns with your goals, lifestyle, and future aspirations. Whether you’re a first-time buyer, upgrading, or investing, our team is here to guide you with expertise and confidence.